“Never invest in something you don’t understand” – Warren Buffett

With an official savings rate of -0.2%, South Africans are not saving at all. This is due to various factors, such as an overall poor savings culture, low incentives to save, or restricted access to savings options. However, the reality is that with an unemployment rate close to 30%, many South Africans cannot save, because they cannot earn an income. According to the Old Mutual Savings Monitor, 40% of South Africans have no form of formal retirement savings. MyTreasury estimated that while 16 million South Africans do have savings accounts, they are emptier than they should be. The South African Reserve Bank estimates that 40% of savings are in accounts that offer exceptionally low interest rates, if any interest at all. Those fortunate South Africans who can save, often do not even know where to start. Well-managed, diversified unit trusts present a good investment option to consider. They are easy to understand and their expected returns are linked to a combination of underlying securities that typically appreciate in real terms over the long term.

What is a unit trust?

A unit trust is a long-only collective investment scheme (CIS) portfolio, being an investment portfolio established under a CIS in securities, regulated by the Collective Investment Schemes Control Act 45 of 2002 (the CISCA). Two or more investors invest money (or other assets) in a unit trust, and hold a participatory interest (e.g. unit, share, other participation) in the unit trust. Investors share the risk and the benefit of investment in proportion to their participatory interest. An exchange traded fund (ETF) is a unit trust that is traded on an exchange.

Unit trust industry facts

- R2.5 tn. market

- Net inflows of ~R120 bn. p.a. (past 5 years)

- ~50 different unit trust managers

- 5 largest unit trust managers include Allan Gray, Coronation, STANLIB, Nedgroup Investments, Ninety One

- >1500 registered unit trusts

- ~90% of unit trusts are actively managed while ~10% follow passive investment strategies

- Average unit trust (excl. ETFs) total expense ratio = 1.45% p.a.

- Average ETF total expense ratio = 0.45% p.a.

- 55% of unit trusts are sold through Linked Investment Services Providers and 95% of these are intermediated by financial advisers

Source: ASISA 31/12/20, STANLIB 30/09/19, etfSA 30/09/19, Soundsolve

Key unit trust features

Regulation

The CISCA regulates the administration, management and sale of CIS portfolios within South Africa.

Safety

- Each CIS is governed by a trust deed, with regulatory supervision by the Financial Services Conduct Authority.

- Investors are protected through the trust property structure, whereby the assets of the trust property are separated from the assets of the CIS manager. The trustee/custodian safeguard the trust property.

Management

The CIS manager is accountable and responsible for all aspects of the administration and management of the unit trusts, including marketing, the buying and selling of participatory interests, keeping records, and making investment decisions.

Diversification

Depending on the investment policy, unit trusts may typically include a combination of South African and foreign listed equities, listed property, bonds, other non-equity securities, money market instruments, and assets in liquid form (cash, or near cash).

Expectations

Unit trusts have clearly defined investment objectives and investment policies, which the investment manager must adhere to. This assists to ensure that the unit trusts are managed in the way that investors have been led to believe.

Liquidity

- Unit trusts and their units are priced daily which enables investors to invest, switch and disinvest their units daily. Settlement is usually completed between 3 and 5 days from the transaction date.

- The unit price is derived from the daily net asset value (NAV), which is a function of the portfolio’s market value, plus income received, minus expenses. The daily unit price is therefore net of all fees and is calculated as the NAV divided by the number of participatory interests in issue.

Transparency

CIS managers must produce, and publish minimum disclosure documents (MDDs), at least quarterly, as at the end of the calendar quarter. MDDs contain key information about the relevant unit trust, including aspects such as the investment policy, objective, risks and risk profile, asset allocation, performance returns, fees and charges. The latest MDDs must be provided to investors before they transact (invest, switch, disinvest), to assist them to make informed decisions.

Fees and Tax

- Material about the unit trusts must include full disclosure of the relevant fees and charges, including the components of the total expense ratio (TER) plus the transaction costs (TC), which equals the total investment charge (TIC).

- CIS managers that are ASISA members must adhere to the ASISA Standard for TER and TC, which prescribes set calculation, disclosure, and reporting requirements.

- Additional fees that may be relevant to investors, such as financial adviser fees, must also be fully disclosed.

- Unit trusts themselves are untaxed and all capital gains, interest, and dividends realised by the investor, are taxed in the hands of the investor.

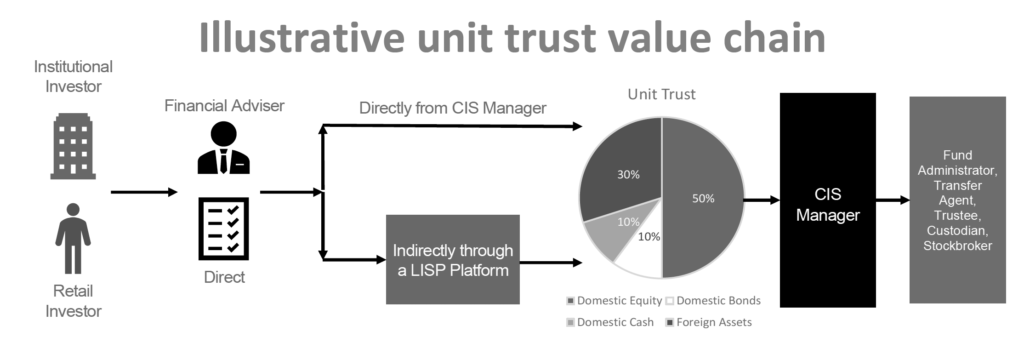

Where can I access a unit trust

Unit trusts are a good investment option to consider and may be suitable for sophisticated, as well as ordinary investors, because they are well structured, governed, and managed. Before considering investing into a unit trust, whether for a discretionary investment or as an underlying investment option within a compulsory financial product (such as a retirement annuity fund, preservation fund, endowment, or living annuity), it is recommended that investors consult a licensed financial adviser for a professional financial needs analysis and investment advice. The unit trust selected should match an investor’s financial needs, risk profile, and investment objective. Investors can access unit trusts directly from a CIS manager, indirectly through a Linked Investment Services Provider (LISP), or through a stockbroker in the case of ETFs.

0 Comments