Unit trust investments, whether made directly or underlying to another financial product like a living annuity, have one certainty, and that is the impact of the fees that you pay. The rest, like your return or the level of volatility, remains completely uncertain.

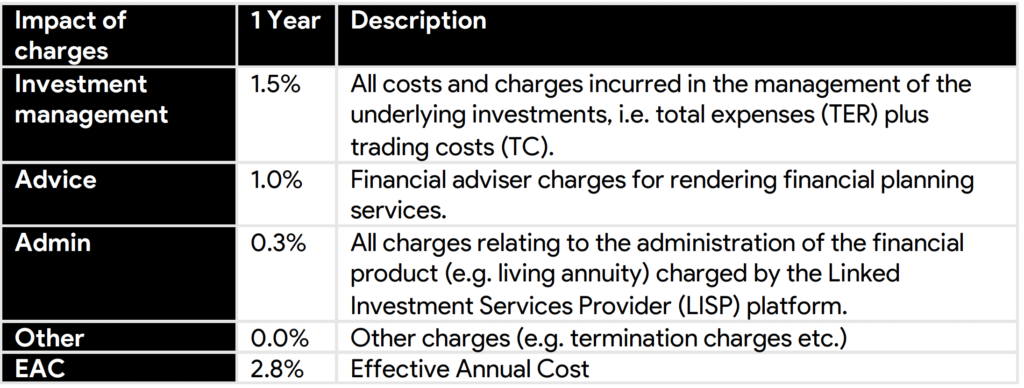

In an environment where returns are becoming increasingly scarce, the importance of understanding and optimizing your investment’s fee structure, has never been more essential as your investment outcome is solely dependent on the return you earn after fees. Gone are the days where investors did not mind, or did not know, that they were paying exorbitant fees. The notion that you pay for what you get is not necessarily true in the case of investments. Members of the Association for Savings and Investment South Africa (ASISA) developed the very welcomed Effective Annual Cost (EAC) measure, which is a standardized disclosure methodology that enables investors to compare the costs most likely to be incurred when investing and holding a financial product, like a living annuity with a unit trust investment underlying. EAC illustration:

In the above illustration, your investment will most likely be 2.8% lower in a year as a direct result of the fees that you will pay. It is strongly recommended that investors obtain professional advice from an accredited financial adviser, to not only ensure that the chosen financial product is appropriate, but that all fees are clearly understood and optimised.

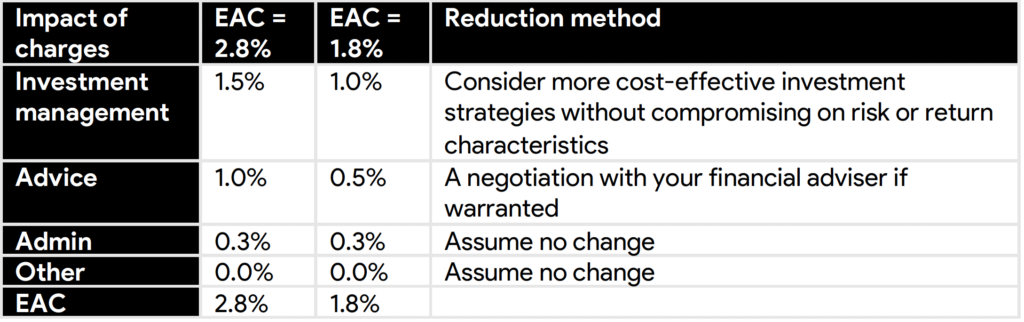

To demonstrate the significant impact a reduction of fees can have on investor outcomes, we compare the end-result for both a higher EAC (2.8%) and lower EAC (1.8%) in the case of a discretionary as well as a compulsory living annuity investment. Firstly, we provide an example of how an EAC can be reduced.

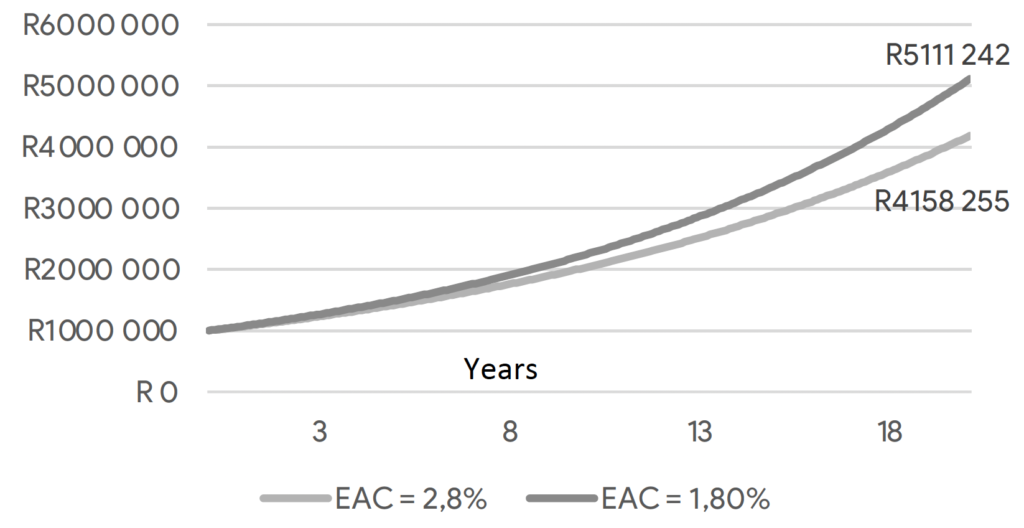

Discretionary investment of R1 000 000 for 20 years

Assuming a constant return of 10% p.a., paying 1% p.a. less in fees, results in a terminal investment value after 20 years of R5 111 242 versus R4 158 255, which is 23% more.

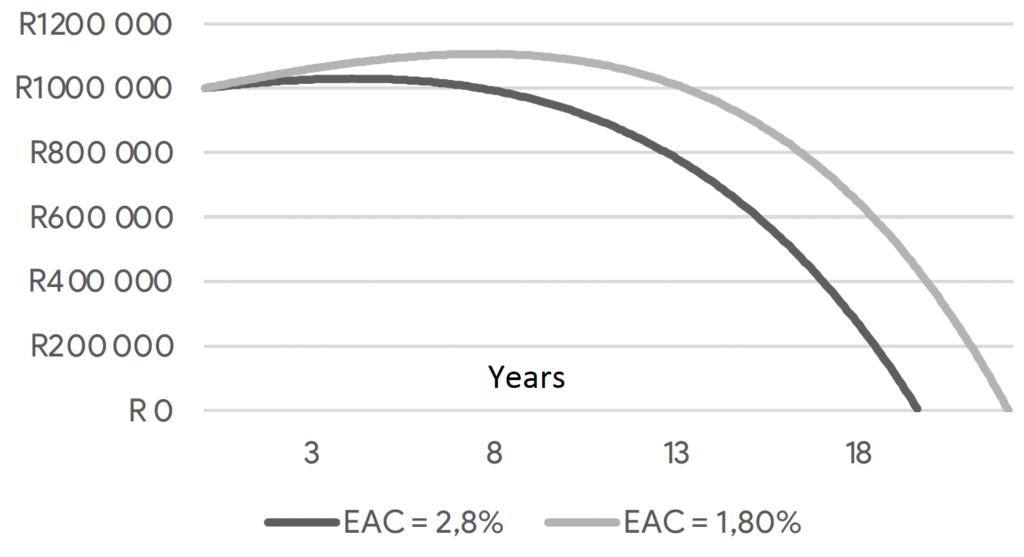

Retiring with R1 000 000 in a living annuity

A person who retires with R1 000 000 growing at a constant return of 10% p.a., who draws a monthly pre-tax income of R5000 growing at an assumed inflation rate of 6% p.a., will run out of money after 19.6 years at an EAC of 2.8%. With an EAC of 1.8% (paying 1% less in fees), the money will only run out two and a half years later (by year 22.1).

Speak to your financial adviser about optimizing your fees.

0 Comments